Most rate headlines continue to miss who actually drives the market.

Many buyers have reached genuine interest rate fatigue.

After six years of COVID change, a boom, aggressive rate rises, and a collapse in borrowing capacity while prices kept rising, many buyers have reached genuine interest rate fatigue.

Some buyers have switched off from trying to pick the perfect moment because the last few years have shown that life and prices keep moving regardless, creating two very different buyer groups.

There’s one group that moves in and out with weekly sentiment. They react quickly to headlines, step back when news turns negative and return slowly when confidence improves.

Then there’s the group that has been trying to act for years. They were relieved not to take on a bigger mortgage when rates spiked, but equally frustrated when their capacity fell 25–30% while prices still rose.

What they could afford in 2020 or 2021 versus what they can afford today is completely different, creating a real fear of falling further behind if they don't act.

This includes upgraders, first-home buyers pushed into action since the October 5% changes, and importantly, workers who froze decisions during job uncertainty or flexibility concerns.

Many of those concerns have now settled, and buyers with secure incomes are once again more comfortable making long-term decisions with greater confidence in their work.

Underneath everything, there is a never-ending demand driven by demographics. Millennials forming families, Gen X upgraders, Baby Boomers holding on to homes, and longer-living, while higher-income migrants continue to arrive.

If combined with construction sector challenges, where developers can’t make projects stack up, there is no meaningful wave of supply coming, with total listings at all-time lows.

Financially strong buyers, such as high-income households, business owners and people with meaningful equity, can act because their position allows them to. While investors are encouraged by rising rents, FOMO fuelled FHBs.

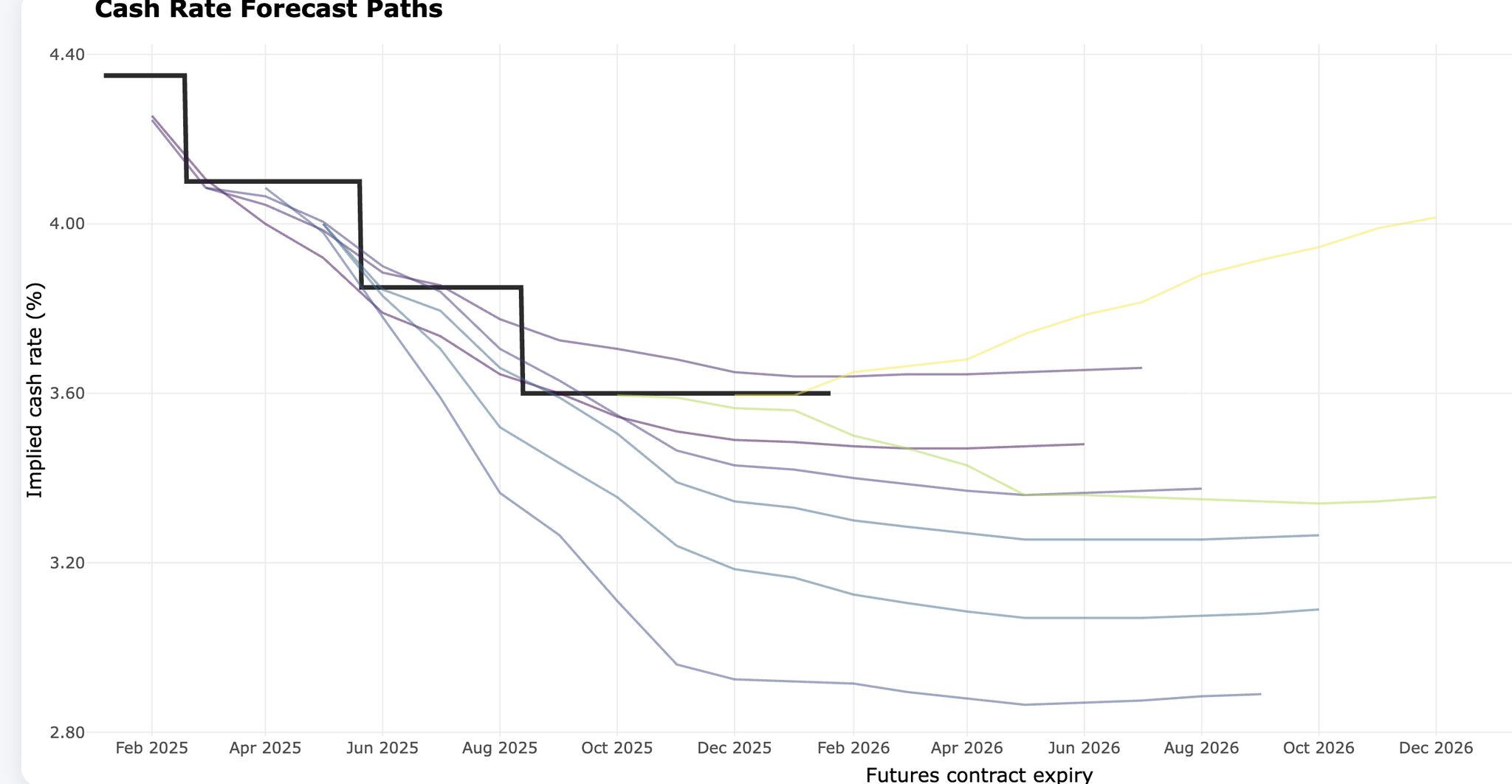

It’s worth remembering how wrong rate expectations have been. In April, markets expected the RBA to fall to around 2.8%. By October, it was 3.6%. By December, it was close to 4.0%. All within eight months. If expectations can swing up this quickly, they can swing down just as fast when the data shifts.

While I don’t expect 2026 to be a runaway market, borrowing capacity is still the handbrake. I do expect this second buyer group to keep buying. They’ve lived with the cost of waiting, and life is driving the decision now, not the next RBA meeting.

The irony, however, is that in 2026, if rates fall, it won’t be easier; it will be harder, with more buyers chasing the same limited stock.

Most people wait for uncertainty to disappear. But when uncertainty disappears, so does the opportunity.

Regret, we believe, is a stronger motivation now than the fear of slightly higher rates, and those who understand that will buy when others are still on the sidelines.

Selected Awards

2025 NSW/ACT Champion

AFG Broker Awards NSW

2025 AFG Champion Broker

Finalist: AFG National Broker Awards

2024 The Adviser

#1 Elite Broker Ranking

2024 MPA

#3 Top 100 Broker Ranking

2024 MFAA Excellence

Finance Broker Business Award