Rates up, what changes?

The attraction of home ownership won't dampen.

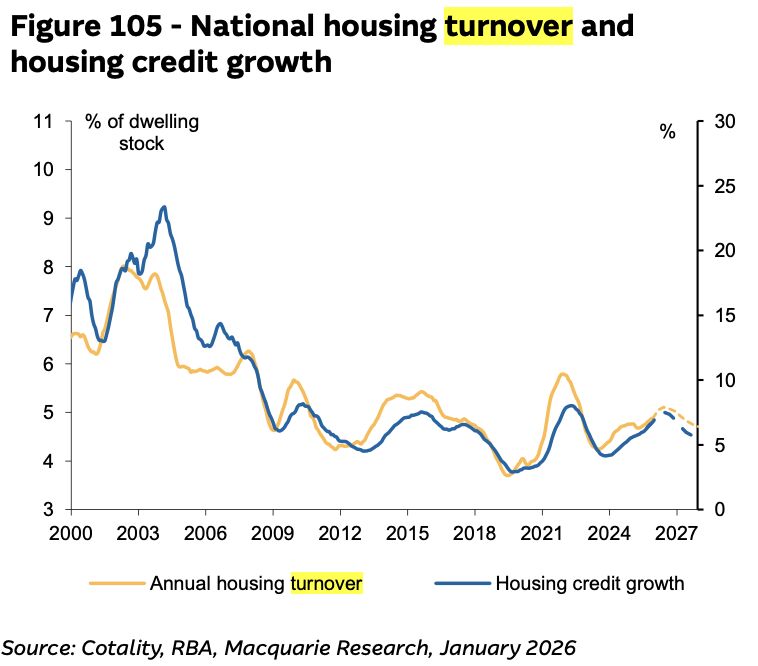

We all know interest rates have gone up, but the right question is what will happen to buyer and seller behaviour.

Residential property is where the vast majority of Australia’s “accessible” wealth is. Our confidence in where the property market is heading drives our spending, borrowing, and investment decisions far more than any other part of the economy.

When the trajectory of rates moved significantly in Q4 2025, the thing that shifted wasn’t prices; in fact, they have still been rising in aggregate, but what people felt comfortable pursuing.

The first point to note for Sydney is that the family upgrader will remain stuck. Higher rates, lower borrowing capacity, limited options and a genuine fear of stretching too far will keep most families on the sidelines.

Only opportunistic, highly confident families will take on more debt at today’s rates, given the real risk of selling first and being pushed into the rental market. This won’t change until the market believes rates are heading down again, but by then, the real opportunity for buyers will have changed as well.

Meanwhile, Brisbane, Perth and Adelaide are running a different race. Supply is so tight that rate movements barely touch sentiment. Buyers in these cities know that if they don’t act, they may not get another chance. These markets don’t need insane demand to hold up; the supply is just that tight. While Melbourne is finally waking up and momentum is building month on month.

First home buyers will not slow down because the 5% deposit scheme is simply too attractive. In a non-hype way, it’s the best scheme for "todays" buyers we’ve ever had.

Investor activity won’t disappear. The continued growth in family net wealth, driven by rising asset prices and wealth transfers, combined with record-high offset balances, creates ongoing opportunities for those who can invest.

I do feel (and hope) they will be far more selective than in recent years.

The word is hopefully out: the hype-driven strategy of “picking the next town” has worn thin, and investors are shifting back toward quality city assets.

Higher rates will catch some highly leveraged investors, especially those who went hard in the last five years or hold poorly performing city apartments to be forced to sell.

So, in my view, the story we will see in 2026 will be the continued funnelling into home ownership.

Crazy incentives for first home buyers, more lending restrictions for investors, potential higher taxes, zoning changing wealthy suburbs, but the sacred CGT-free status of the family home will stay politically untouchable and attractive as a safe-haven for wealth.

In the short term, upgrader markets remain stuck, many markets grow while rental tighten, pent-up builds for rate cut expectations to come back.

When they do the part of the market that have underperformed the most, especially the mid-to-upper segments, will be the ones that grow the fastest.

Selected Awards

2025 NSW/ACT Champion

AFG Broker Awards NSW

2025 AFG Champion Broker

Finalist: AFG National Broker Awards

2024 The Adviser

#1 Elite Broker Ranking

2024 MPA

#3 Top 100 Broker Ranking

2024 MFAA Excellence

Finance Broker Business Award