4 reasons why First Home Buyers should not miss the 5% Deposit Scheme opportunity

The window to act is closing, fast.

.png)

On 1 October 2025, just one month away, the 5% deposit scheme will change dramatically.

Those who are in the market now and best prepare will benefit the most, while those who wait until October will face intense competition to catch the wave, and an opportunity cost could be a lot in just weeks, not months.

1. No more income limits

Right now, anyone earning over $125,000 (or $200,000 as a couple) is locked out. From October, that barrier disappears. Whether your household income is $150,000, $250,000, or $500,000, you’ll be able to buy your first home with just a 5% deposit, no LMI, and on competitive rates.

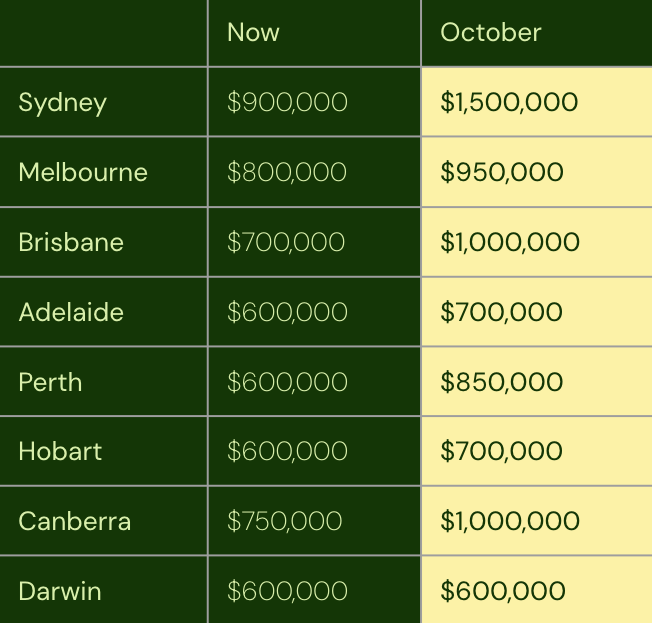

2. Higher price caps

As you can see below, there are some significant increases. In NSW, the cap jumps from $900,000 to $1.5 million. That shifts the scheme from “entry-level compromise” to “genuine family home and quality investment.” FHBs will finally have access to the suburbs and properties they actually want to stay in long-term.

3. Bigger borrowing capacity

By January, we could see 2–3 more rate cuts on top of the three already delivered. Even without wage growth, HECS reforms, or APRA changes, that alone points to at least a 15% lift in borrowing power in just 12 months.

4. Market momentum

Markets move fast. After the consolidation and wage inflation of 2022–2025, conditions are set for the next leg up in stretching affordability. If the RBA pushes rates below 3%, confidence will explode, and momentum could drive prices higher, quickly.

The time to prepare isn’t October, it’s now. You want to be ready to move the ASAP. That also means thinking about Plan B and C alongside your dream property. While everyone else piles into the same hotspots, you might find better opportunities in less obvious locations where competition is less. In these markets, the key is to buy a quality asset fast, and being open to multiple options will increase your chances. For many FHBs, this is the first real chance to buy without the usual 15% savings hurdle and the pain of LMI while taking advantage of a broken system that will undoubtedly push prices higher.

Selected Awards

2025 NSW/ACT Champion

AFG Broker Awards NSW

2025 AFG Champion Broker

Finalist: AFG National Broker Awards

2024 The Adviser

#1 Elite Broker Ranking

2024 MPA

#3 Top 100 Broker Ranking

2024 MFAA Excellence

Finance Broker Business Award