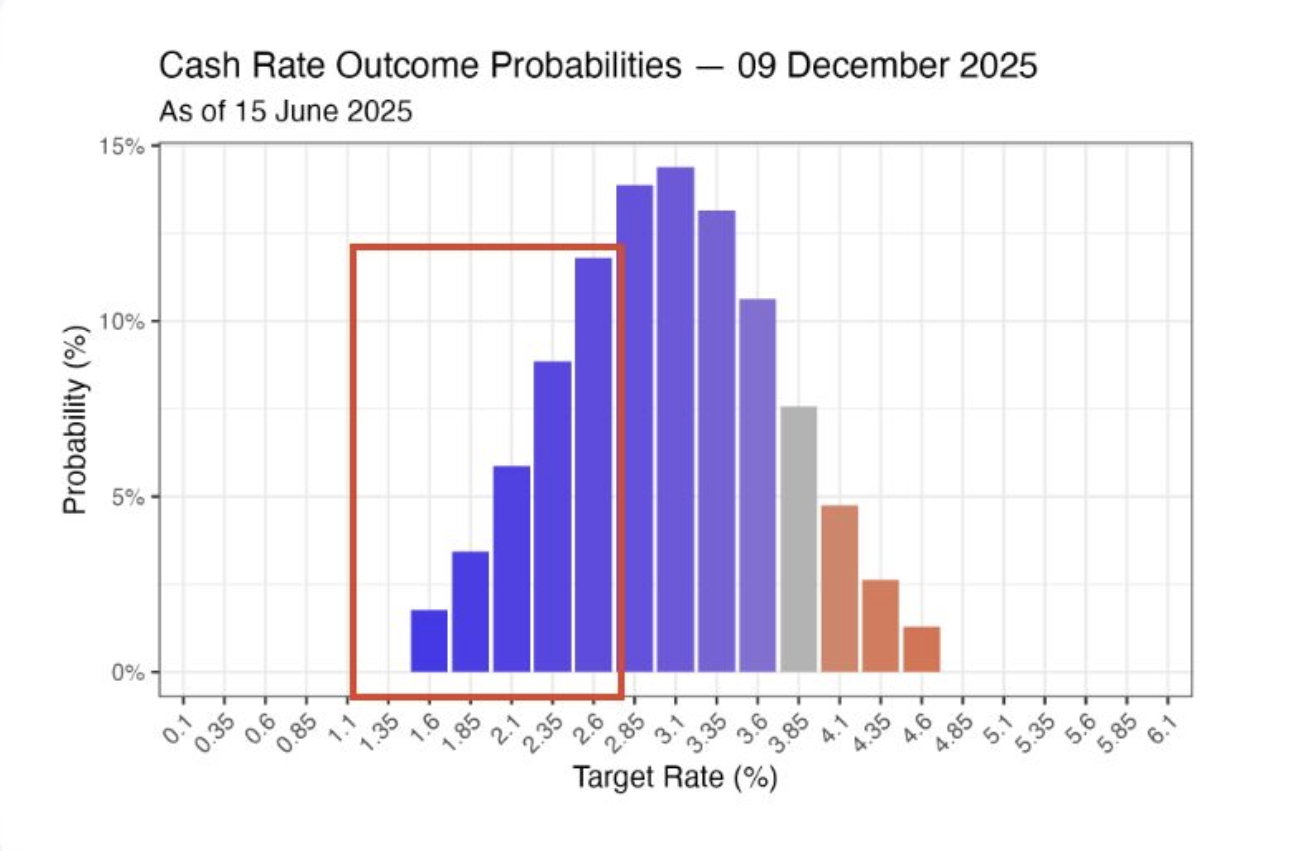

What if the RBA rate goes to 2%?

What if the RBA rate goes to 2%?

Recently, our new clients have come to us believing that more cuts are coming and are already factoring in further reductions in their confidence in buying.

New data continues to flood in, and expectations of slower growth and tighter inflation are gaining steam. The question is whether the RBA rhetoric might shift to actively stimulating the economy?

While current expectations only see rates going to 3%, what happens if rate expectations shift to 2.5% or even 2%?

In his last AFR article, Chris Joye mentioned that the current world conflict further pressures the need for cuts. Even the strongest interest rate bears such as Warren Hogan, who initially thought rates needed to go higher, are flipping, saying, "There is no need to wait."

We all have a recency bias, fearing where rates could have gone and the pressure it would have put households under. Loss aversion holds us back, as potential losses are greater than gains.

However, only 4 years ago, property market confidence was sky-high.

The Westpac Index of House Price Expectations recently surged 7% to 166.5 - the highest level since 2013. Consumer sentiment is shifting toward optimism, yet many buyers remain paralysed by "what if" scenarios of the past.

Even with current expectations of rates falling to 3%, the market expects house prices to be 5-10% higher by year-end.

It reminds me of markets when risk-to-reward makes sense, similar to investing heavily in shares after significant declines.

While the property market doesn't function on the same fundamentals and starting price, falling rates and increasing borrowing capacity are highly demand-stimulating.

The primary concern holding prices back would be an oversupply of listings. However, total listings are way down on 5-year averages, which are way down on 10-year averages. We have a very tight property market, not just for buying but also for renting.

If we agree that the general rate trajectory is down, we are only unsure how deep the RBA will cut; the real downside risk is slightly larger mortgage repayments than expected. The property market prices showed resilience at 4.3% rates; why wouldn't it stay resilient if RBA rates stopped at 3.3%?

Remember the 2019 election when Labor expected to win but didn't? The property market immediately went into a tear. Similarly, after the initial COVID fear, when rates plummeted, property boomed due to expectations of lower rates for longer.

If inflation is truly back in the bottle, the question becomes: Would you want to upgrade or invest at rates around home loan rates at 5%?

But more broadly, if home loan rates crash closer to 4% or lower, are you okay with missing out on the considerable impact of market growth?

Whether upgrading or investing, now could be a time when there is limited downside with substantial upside. The question isn't whether rates will fall but whether you will benefit if they fall deeper than anyone expects.

Selected Awards

2025 NSW/ACT Champion

AFG Broker Awards NSW

2025 AFG Champion Broker

Finalist: AFG National Broker Awards

2024 The Adviser

#1 Elite Broker Ranking

2024 MPA

#3 Top 100 Broker Ranking

2024 MFAA Excellence

Finance Broker Business Award